Renter Affordability Statistics As of Q3 in 2020

Return to Blog

Published 12/05/2020

The housing market has had a spectacular recovery since May, but at the same time, home prices have been surging. This post will explore the levels of difficulty for renters to achieve the dream of homeownership with the data presented by the National Association of Realtors.

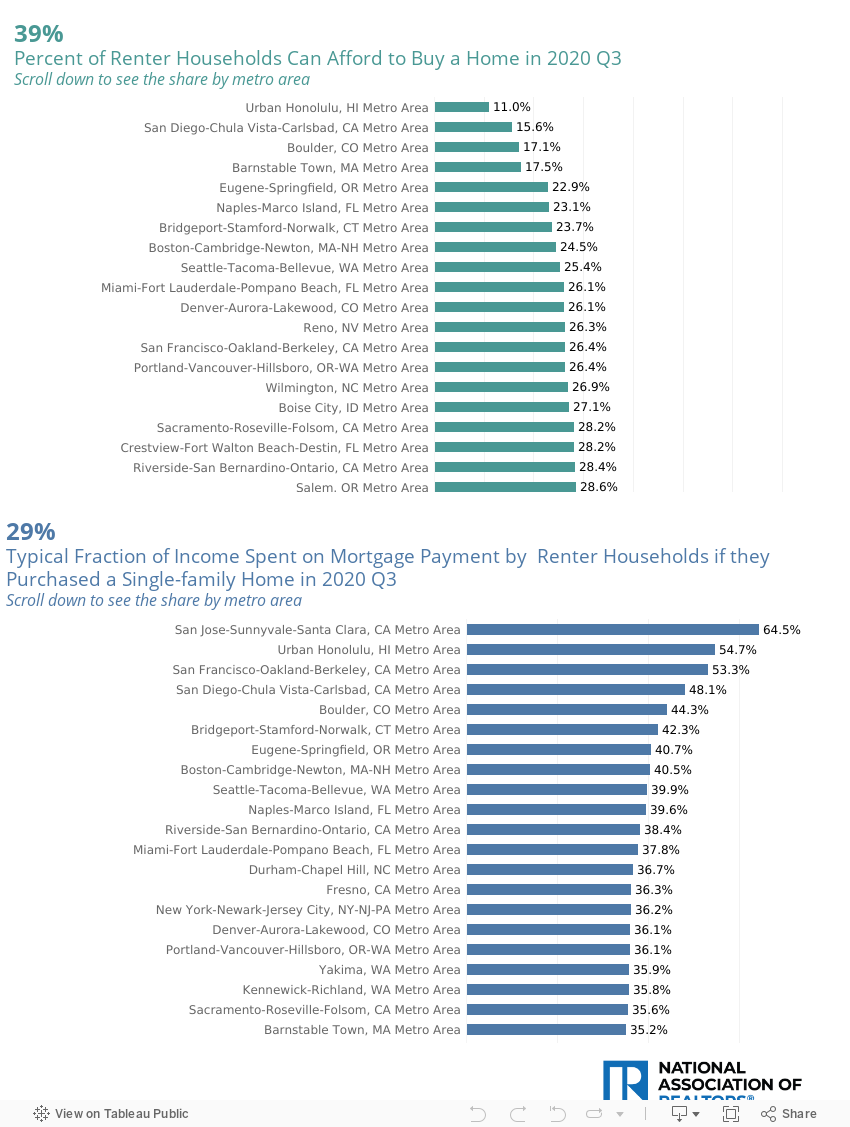

38% of renters can afford to buy a home but need 13 years of savings to make a 10% down payment:

As mortgage rates have fallen and incomes have increased. The fraction of renters who can afford to purchase a home has increased from 33% in 2018 to 39% as of 2020. However, as of 2020 Q3, the fraction of renters that can afford a home has increased since 2018 to 39%.

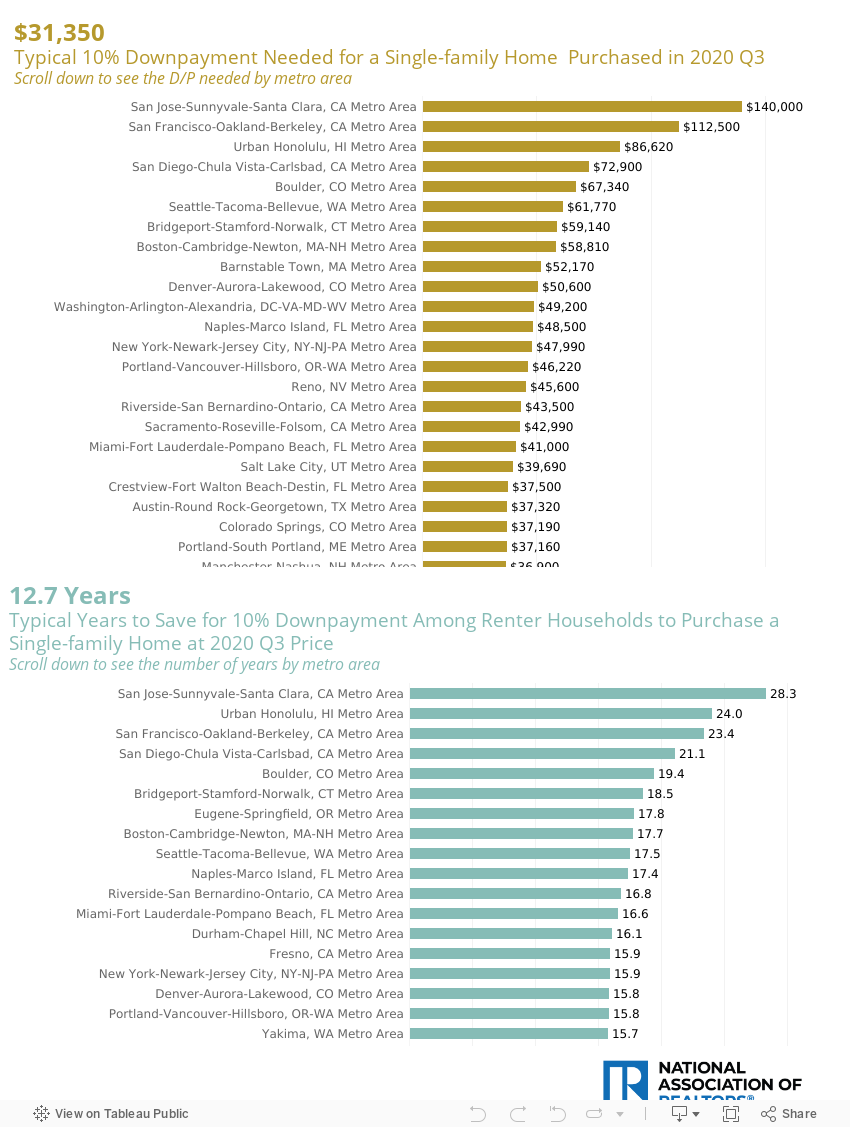

Although achieving the dream of homeownership is still challenging for renters in terms of paying the monthly mortgage (mortgage payment accounts for 29% of income.) Which totals to a down payment of 10%, about $31,350 (at current median single-family sales price) — which is equivalent to 13 years of savings.

A renter will typically spend 29% of income on a mortgage payment:

While a home purchase has become more affordable, a renter with a family income of $49,242 or less will not be able to afford a typical single-family home valued at 313,500 as of 2020 Q3. If a renter purchased a single-family home in Q3 of 2020, the mortgage payment accounts for 29% of income, above the 25% threshold.

Another way to assess affordability is to compare the median family income to the income needed so that the renter will not spend more than 25% of income on a mortgage payment (qualifying income). In 2020 Q3, the estimated median family income of a renter was $49,242, which is below the level of income needed to afford a home, at $57,172 ( so the home affordability index is 86.1). In comparison, current homeowners whose family income is about double the median family income of renters have more than the income needed to purchase a typical single-family home (so the home affordability index is 173.4).

A renter will need about $30,000 for a 10% down payment and 13 years of savings:

According to NAR’s 2020 Profile of Home Buyers and Sellers, first-time buyers typically financed 93% of their home or put down 7% for a down payment. NAR’s monthly Realtors® Confidence Index survey places the average down payment among first-time buyers at around 9% to 10%. While a 3% FHA loan is available, first-time buyers are putting down a higher down payment, presumably to save on the monthly mortgage payment.

Due to the long time to save for a down payment, President Biden’s homebuyer tax credit will help speed up the home purchase for many renters and enable them to gain housing wealth from the home price appreciation earlier. But this will mean that supply has to increase, meaning prices don’t also rise even more amid tight supply conditions.

If you have questions about how you can develop or refine your homeownership plan, contact Darryl Glass today. For assistance with all home buying and selling needs, please call (510) 500-7531 or email dglass@adventpropertiesinc.com.